Last week’s market activity was shaped by several significant themes. Firstly, the Japanese Yen’s rapid decline caught market participants off guard. The sell-off was exacerbated by what many considered tepid verbal interventions from Japanese officials. Current momentum suggests that the Yen’s free fall is far from over. The key is whether Japan will step up with stronger actions, or at least words, as Yen approaches 160 mark against the greenback.

Secondly, investor confidence in the US showed remarkable resilience. Despite economic data suggesting that Fed would further delay interest rate cuts, US markets have adapted to this new outlook well. There is a growing sentiment that robust economic data will continue to be received positively, reinforcing the adage that “good news is good news.”

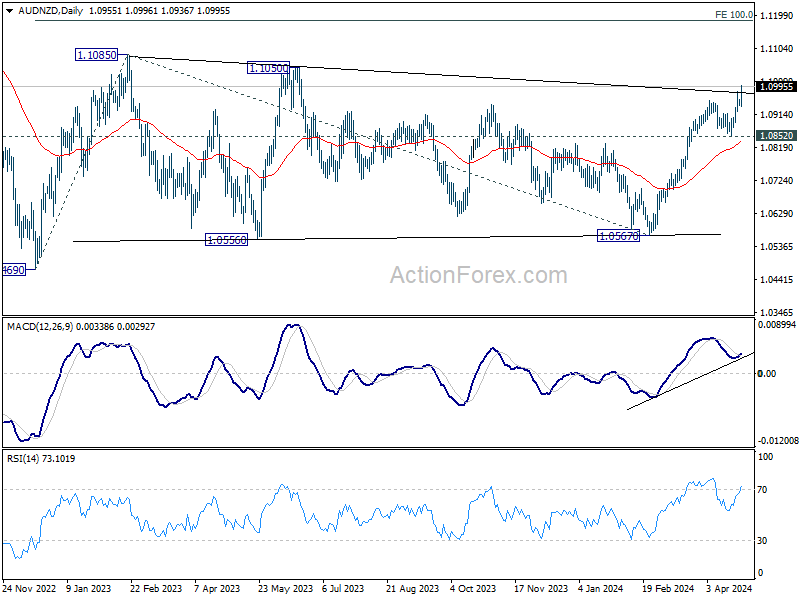

Thirdly, Australian Dollar benefited not only from strong domestic economic and inflation data but also from renewed optimism towards China’s economic recovery. The substantial rally in Hong Kong stocks has mirrored this positive sentiment. Should this positive sentiment towards China’s economy solidify into a stable trend, this could spell further upside for Aussie.

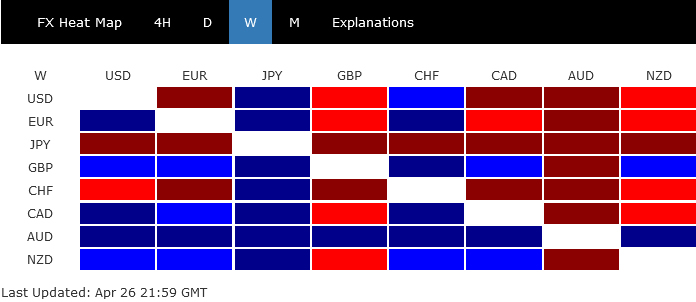

In a broader view of the currency markets, Yen concluded the week as the weakest performer, followed by Swiss Franc and Dollar. On the other end of the spectrum, Australian Dollar emerged as the top performer, followed by British Pound and New Zealand Dollar. Euro and Canadian Dollar occupied the middle ground.

Strong Finish for US Stocks After Volatile Week; Market Accepts Diminished Prospects for Fed Cuts

US stock markets ended a notably turbulent week on a high note, with major indices recording their best performances since November. S&P 500 rose by 2.7%, while NASDAQ saw an impressive 4.2% gain. DOW also climbed, albeit more modestly, by 0.7%. Some analysis attributed the rally to stellar earnings reports from tech giants and AI competitors Alphabet and Microsoft. But it’s important to note the resilience of investor sentiment against the backdrop of mixed economic indicators.

Investors initially braced for impact following the release of weaker-than-expected Q1 GDP growth figures and higher-than-anticipated inflation data. However, the market’s resilience suggests robust underlying confidence, supported by expectations of continued strong consumer spending. The economy is anticipated to be bolstered by consumption, even amidst elevated inflation and interest rate levels. This consumer resilience suggests sustained demand that could keep inflation at elevated levels, keep Fed’s hands off from aggressive monetary policy easing.

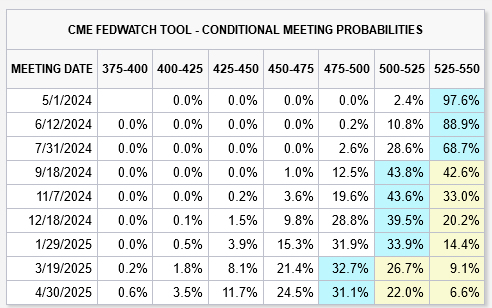

The overall market dynamics argues that expectation of fewer Fed rate cut, or even no cut this year at all, is well priced in, and absorbed by investors. According to Fed fund futures, the probability of two rate cuts this year is now around 40%, with 20% chance that rates will remain unchanged.

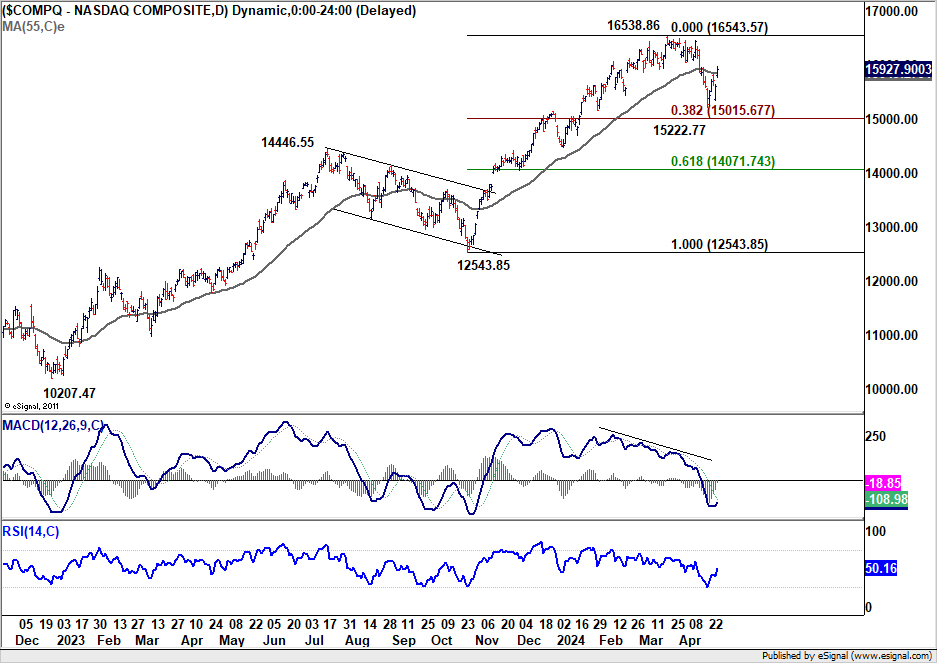

NASDAQ’s break 55 D EMA argues that pull back from 16538.86 has completed at 15222.77. Price actions from 16538.86 are likely developing into a sideway consolidation pattern to rise from 12543.83 only. The range should be set between 38.2% retracement of 12543.85 to 16538.86 at 15015.67 and 16538.86, or in short, between 15000 and 16500.

10-year yield’s rally from 3.785 is staying to lose some upside momentum even though there is no clear sign of topping yet. While further rally remain in favor, upside should be capped below 4.997 high. Break of 4.568 will bring pullback to 55 D EMA (now at 4.383) first. It’s a highly unlikely scenario for now, but upside re-acceleration in 10-year yield and break of 4.997 resistance could be a sign that inflation in the US is getting out of control again, which would force Fed to tighten again.

Dollar index retreated after failing to break through rising channel resistance. But price actions from are so far corrective. Outlook will stay bullish as long as 104.97 resistance holds. Rise from 100.61, as the third leg of the pattern from 99.57, is still expected to extend to 107.34 resistance, and possibly further to 100% projection of 99.57 to 107.34 from 100.61 at 108.38.

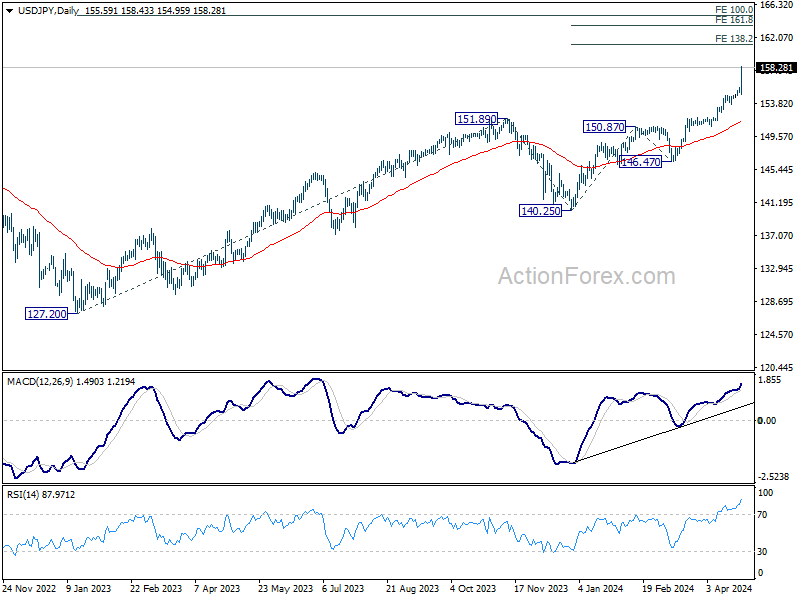

Yen’s Accelerated Decline Exposes Inadequate Resolve for Currency Intervention

Another major theme of the currency markets was the intensified broad-based selloff in Japanese Yen. The decline briefly paused before BoJ meeting but the downward spirally quickly resumed afterwards. The post-meeting comments from Governor Kazuo Ueda highlighted that the weakening Yen has yet to significantly impact Japan’s inflationary pressures. This observation has led to speculation that the Japanese government may refrain from intervening in the currency markets for now.

This steep depreciation is noteworthy especially considering the recent trilateral meeting between Japan, South Korea, and US just a week ago, which addressed the slump of Asian currencies. The lack of resolve for coordinated market intervention was tested and proven by market developments. Further, the stance was reinforced by US Treasury Secretary Janet Yellen’s comments, as she indicated that the US expects currency market interventions to be “rare” and only reserved for periods of “excessive volatility.”

For the near term, USD/JPY’s rally is in progress to 138.2% projection of 140.25 to 150.87 from 146.47 at 161.14. Attentions will be on whether Japan would step up verbal intervention near 160, or even back up with actual actions. If not, next target would be 161.8% projection at 163.65.

Nikkei traders are so far unimpressed by the free fall in Yen. While a weaker Yen would boost exports and tourism, it would hurt imports in particular energy, and squeeze margins out of businesses. The next few days could be important for the technical development. If Nikkei could bounce from current level and break through 55 D EMA (now at 38349.15) decisively, that would suggest that price actions from 41087.75 is merely developing into a sideway pattern, rather than a large scale bearish reversal. Such development would be a relief to both the government and BoJ.

Aussie Surges Amid RBA Rate Cut Delays and Renewed China Optimism

Australian Dollar emerged as the standout performer this week, buoyed by a combination of robust economic indicators and growing optimism around the Chinese economy’s recovery.

Early in the week, strong PMI data provided a solid foundation, suggesting acceleration in Australia’s GDP growth in Q2. The increasing economic activity also comes with its challenges, particularly as inflation has not on sustained path back to RBA’s target band. This situation has raised discussion among analysts the possibility of further tightening by RBA.

Meanwhile, Q1 CPI data showed that disinflation progress has been rather dissatisfactory. March’s monthly CPI even accelerated, hinting at risk of resurgence in inflation. Analysts have subsequently adjusted their forecasts, pushing back the timeline for an anticipated RBA rate cut from the third to the fourth quarter of the year, some even suggesting it might be delayed further.

Adding to the positive outlook for Aussie is renewed confidence in the Chinese economy, Australia’s major trading partner. This optimism is palpably reflected in the performance of Hong Kong’s stock market. HSI powered through medium term channel resistance to close at 17651.15. Immediate focus is now on 38.2% retracement of 22700.85 to 14794.16 at 17814.51. Decisive break there will raise that chance that HSI is already reversing the downtrend from 22700.85. Further rise should then be seen to 61.8% retracement at 19680.49 and above.

AUD/NZD’s rally from 1.05670 resumed and even broke through medium term trendline resistance. The development is strengthening the case that sideway consolidation from 1.1085 has completed with three waves to 1.0567. Near term outlook will now stay bullish as long as 1.0852 support holds. Next target is 100% projection of 1.0469 to 1.1085 from 1.0567 at 1.1183.

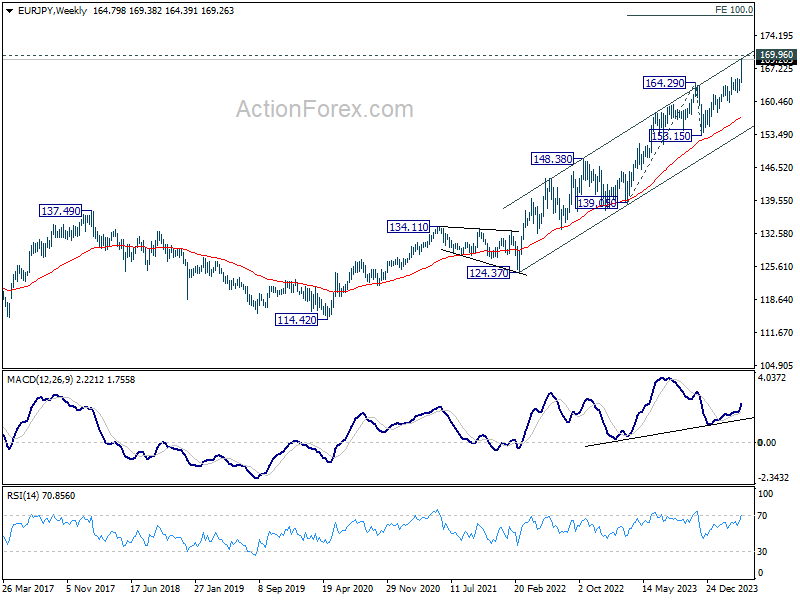

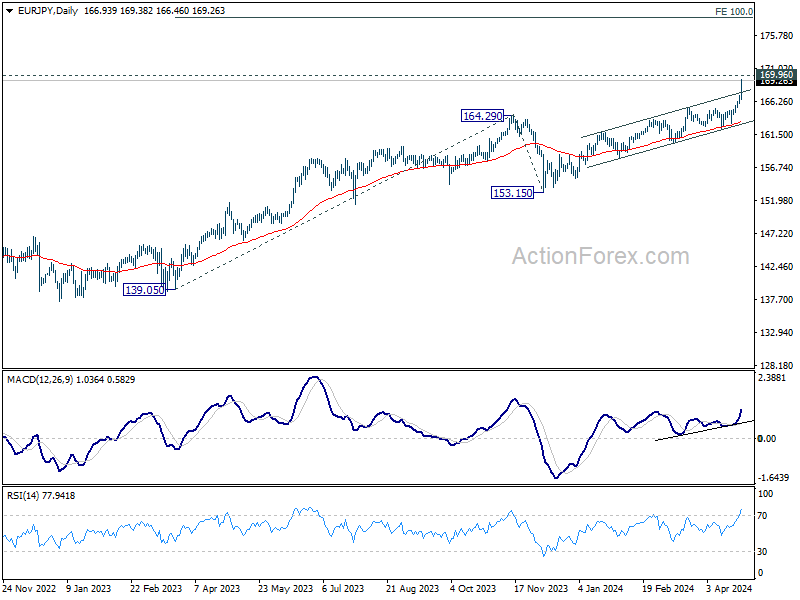

EUR/JPY Weekly Outlook

EUR/JPY’s up trend resumed last week and accelerated to as high as 169.38. Initial bias remains on the upside this week. Next target is 169.96 high the downside, below 167.76 minor support will turn intraday bias neutral and bring consolidations. But pull back should be contained well above 165.33 resistance turned support to bring another rally.

In the bigger picture, current rally is part of the up trend from 114.42 (2020 low), which is still in progress. Next target is 169.96 (2008 high). Decisive break there will pave the way to 100% projection of 139.05 to 164.29 from 153.15 at 178.39. On the downside, break of 162.26 support is needed to be the first sign of medium term topping. Otherwise, outlook will stay bullish in case of retreat.

In the long term picture, rise from 114.42 (2020 low) is seen as the third leg of the whole up trend from 94.11 (2012 low). Next target is 100% projection of 94.11 to 149.76 from 114.42 at 170.07 which is close to 169.96 (2008 high). Firm break there will target 138.2% projection at 191.32. This will remain the favored case as long as 153.15 support holds.