Dollar is overwhelmingly the worst performer for the week, after yesterday’s post-CPI selloff. Yen is the strongest one, with help from the steep decline in US yields too. European majors follow as next strongest, with Swiss Franc having an upper hand against Euro and Sterling. While US stocks surged and Asia followed, commodity currencies are overall just mixed for the week.

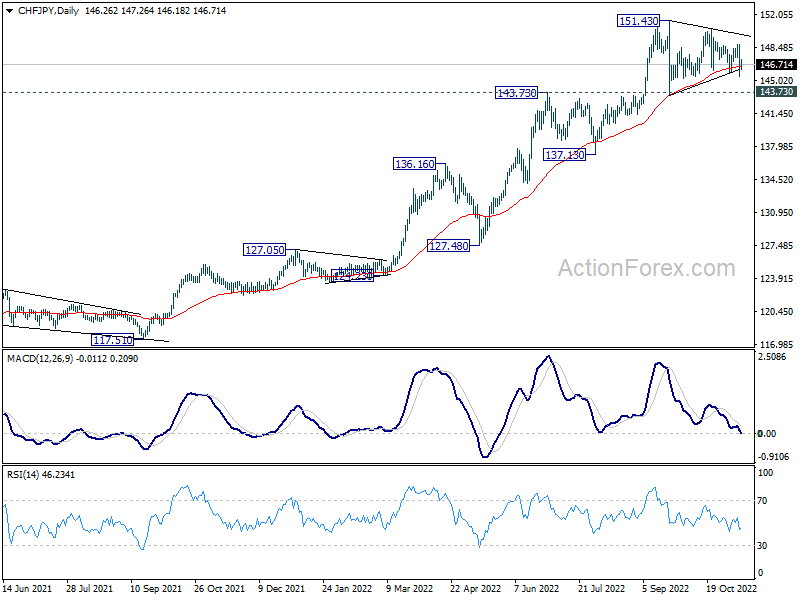

Technically, one question now is whether Yen could build on current rebound to stage a broad-based medium-term rally, even as a corrective move. Some attention could be paid to CHF/JPY to monitor the development. Sustained trading below 55 day EMA (now at 146.50) will be the first sign of a reversal. Firm break of 143.73 resistance turned support should confirm that CHF/JPY is already in a medium term correction, at least, and should that 137.13 support and possibly below. That would be a sign of more Yen strength elsewhere.

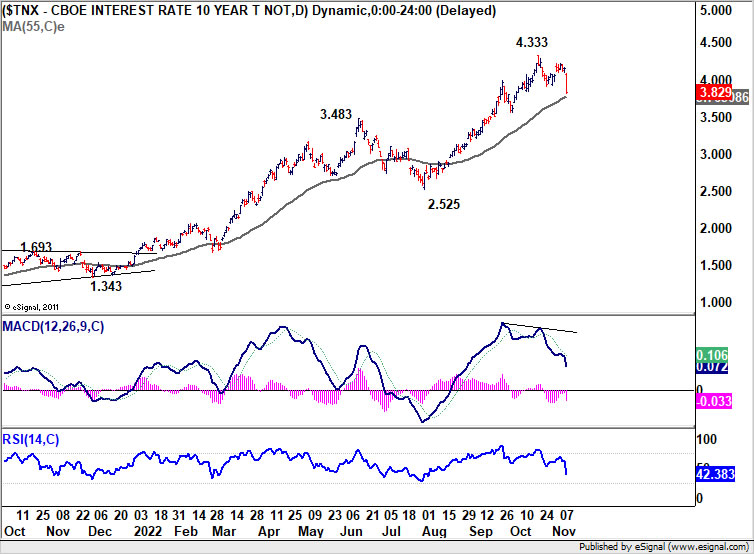

In Asia, Nikkei rose 2.98%. Hong Kong HSI is up 7.25%. China Shanghai SSE is up 2.11%. Singapore Strait Times is up 1.65%. Japan 10-year JGB yield is down -0.0082 at 0.238. Overnight, DOW rose 3.70%. S&P 500 rose 5.54%. Even NASDAQ rose 7.35%. 10-year yield dropped sharply by -0.322 to 3.829.

Fed Daly: One month does not a victory make

San Francisco Fed President Mary Daly said yesterday that the slowdown in inflation was “goods news”. Yet, “one month does not a victory make.”

“We have to be resolute to bring inflation down; we’re united in that commitment,” she said. “It’s raising the rate and then holding it for a length of time that is sufficient to bring inflation reliably back to 2%.”

“I would rather move a little bit higher and have to come back then to move a little bit less high and to then tell people we’re going to go higher, because at some point it does seep into inflation expectations,” Daly said.

At the same time, she said, “I don’t want to be over tightening to the point where we throw the economy into a sharp recession, but if we are talking about a rate hike on either side, I want to fully get inflation sustainably down to 2% on average.”

Fed Mester: There continue to be some upside risks to inflation forecast

Cleveland Fed President Loretta Mester yesterday’s October CPI report “suggests some easing in overall and core inflation.” However, “there continue to be some upside risks to the inflation forecast.” She expects to see a “meaningful” decrease in inflationary pressures next year and after, with CPI back to 2% target by 2025.

“Given the current level of inflation, its broad-based nature, and its persistence, I believe monetary policy will need to become more restrictive and remain restrictive for a while in order to put inflation on a sustainable downward path to 2%,” she said.

“Despite the moves we have made so far, given that inflation has consistently proven to be more persistent than expected and there are significant costs of continued high inflation, I currently view the larger risks as coming from tightening too little.”

Fed George urges steady and deliberate approach to raising policy rate

Kansas City Fed President Esther George said yesterday, “I continue to see several advantages for a steady and deliberate approach to raising the policy rate.”

“Without question, monetary policy must respond decisively to high inflation to avoid embedding expectations of future inflation,” she said. “A more measured approached to rate increases may be particularly useful as policymakers judge the economy’s response to higher rates”.

“As the tightening cycle continues, now is a particularly important time to avoid unduly contributing to financial market volatility, especially as volatility stresses market liquidity with the potential to complicate balance sheet run-off plans,” George said.

“The degree of tightening necessary will only be determined by observing the dynamics of the economy and inflation and cannot be predetermined by theory or pre-pandemic benchmarks,” George said.

BoC Macklem: We need to rebalance the labor market

BoC Governor Tiff Macklem said yesterday, “We need to rebalance the labour market… This will be a difficult adjustment. We want to do this in the best way possible for Canadian workers and businesses.”

“The unemployment rate in June hit a record low [of 4.9%] – and while that seems like a good thing, it is not sustainable,” he explained. “The tightness in the labour market is a symptom of the general imbalance between demand and supply that is fuelling inflation and hurting all Canadians.”

SNB Maechler: Further rate hikes may be necessary

SNB board member Andrea Maechler said an in interview, “it is not out of the question that, based on new figures and developments, further rate hikes may be necessary to ensure price stability in the medium term.”

“So it is really important to make an overall assessment with the figures we will have in December,” she said.

Regarding inflation, “on the one hand, a single figure will never allow us to claim victory, and on the other hand, it is still 3%, far from the range that we associate with price stability,” Maechler said.”We will claim victory when inflation settles below 2% on a sustainable basis.”

Looking ahead

UK data will take center stage today with GDP, production and trade balance. Germany will release CPI final. US will release U of Michigan consumer sentiment, which could also move the markets.

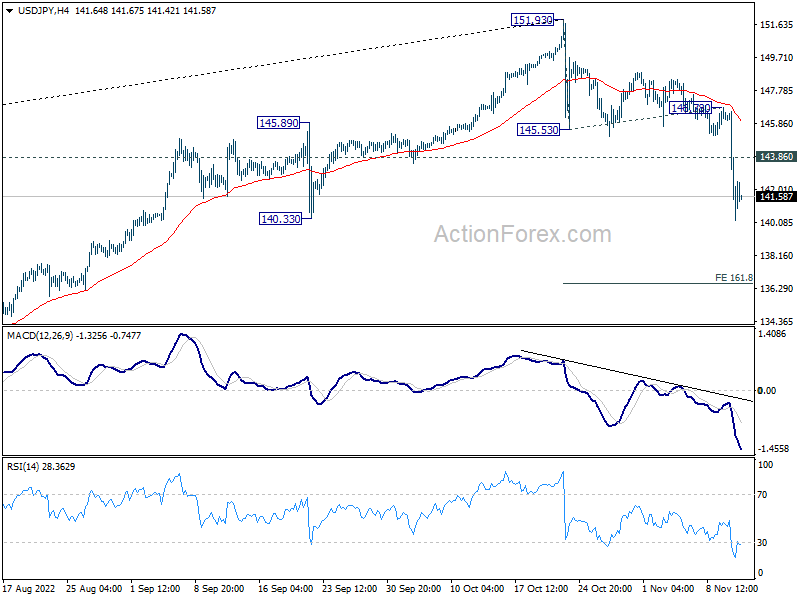

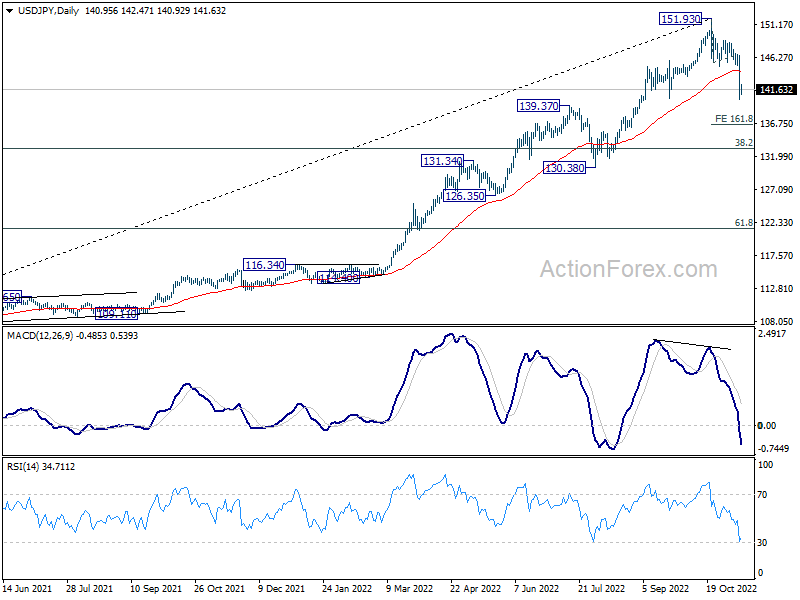

USD/JPY Daily Outlook

Daily Pivots: (S1) 138.58; (P) 142.59; (R1) 144.96; More…

USD/JPY’s correction from 151.93 is in progress and intraday bias stays on the downside. Next target is 161.8% projection of 151.93 to 145.53 from 146.78 at 136.42. On the upside, above 143.86 minor resistance will turn bias neutral and bring consolidations first, before staying another fall.

In the bigger picture, a medium term top should be formed at 151.93. Fall from there is correcting larger up trend from 102.58. It’s too early to call for bearish trend reversal. But even as a corrective move, such decline should target 38.2% retracement of 102.58 to 151.93 at 133.07, or further to 55 week EMA (now at 130.73).

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | PPI Y/Y Oct | 9.10% | 8.80% | 9.70% | |

| 07:00 | EUR | Germany CPI M/M Oct F | 0.90% | 0.90% | ||

| 07:00 | EUR | Germany CPI Y/Y Oct F | 10.40% | 10.40% | ||

| 07:00 | GBP | GDP M/M Sep | -0.40% | -0.30% | ||

| 07:00 | GBP | GDP Q/Q Q3 P | -0.50% | 0.20% | ||

| 07:00 | GBP | Industrial Production M/M Sep | -0.30% | -1.80% | ||

| 07:00 | GBP | Industrial Production Y/Y Sep | -4.30% | -5.20% | ||

| 07:00 | GBP | Manufacturing Production M/M Sep | -0.40% | -1.60% | ||

| 07:00 | GBP | Manufacturing Production Y/Y Sep | -6.60% | -6.70% | ||

| 07:00 | GBP | Index of Services 3M/3M Sep | -0.20% | -0.10% | ||

| 07:00 | GBP | Goods Trade Balance (EUR) Sep | 18.6B | -19.3B | ||

| 13:00 | GBP | NIESR GDP Estimate Oct | -0.30% | |||

| 15:00 | USD | Michigan Consumer Sentiment Index Nov P | 59.7 | 59.9 |