Dollar came under pressure against European currencies following release of US non-farm payroll report, despite the data being robust overall. In contrast, the greenback held firm against Yen and Aussie, while advancing against Loonie, with the latter pressured by surprisingly large increase in Canada’s unemployment rate, signaling sharp loosening in its labor market.

The NFP report showed job growth exceeding the average of the prior 12 months, while earnings growth beat expectations, underscoring resilience in the U.S. labor market. The slight uptick in the unemployment rate, while a minor blemish, didn’t significantly alter market sentiment. Overall, the data is not strong enough to deter Fed from delivering another 25bps rate cut at its December meeting. Market sentiment has shifted decisively, with Fed funds futures now pricing in more than 90% chance of a cut, up sharply from 71% just a day earlier.

Reactions in other markets to NFP report have been relatively subdued, with stock futures posting modest gains. US 10-year Treasury yield dipped slightly but lacked the momentum to decisively break through 4.15% level yet. With much of the immediate reaction to the payroll data absorbed, market activity might taper off as traders square positions ahead of next week.

For the week, Swiss Franc is leading as the strongest performer, followed by Sterling and the Euro. Australian Dollar remains the weakest, with Kiwi and Loonie trailing behind. Dollar and Yen are positioned in the middle of the pack.

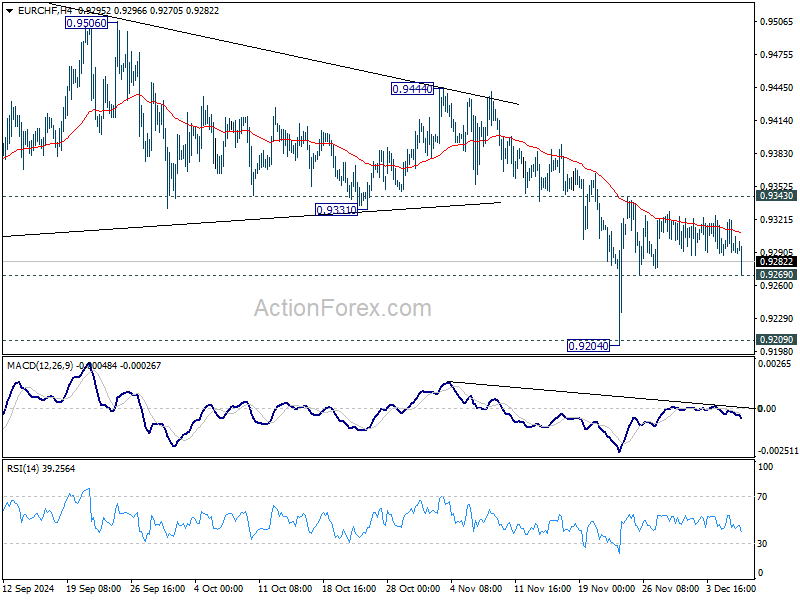

Technically, EUR/CHF has been repeatedly rejected by falling 55 4H EMA, which keeps near term outlook bearish. A focus now is whether the cross would break through 0.9269 support and lose below before the week ends. If released, that could set up further selloff in Euro, and push EUR/CHF for a retest on 0.9204 low next week.

In Europe, at the time of writing, FTSE is up 0.02%. DAX is up 0.28%. CAC is up 1.46%. UK 10-year yield is down -0.016 at 4.272. Germany 10-year yield is down -0.002 at 2.114. Earlier in Asia, Nikkei fell -0.77%. Hong Kong HSI rose 1.56%. China Shanghai SSE rose 1.05%. Singapore Strait Times fell -0.69%. Japan 10-year JGB yield fell -0.0195 to 1.053.

US NFP grows 227k in Nov, unemployment rate rises to 4.2%

US non-farm payroll employment grew 227k in November, close to expectation of 218k. That’s notably higher than the average of 186k monthly growth over the prior 12 months.

Unemployment rate rose from 4.1% to 4.2%, above expectation of 4.1%. Labor force participation rate was at 62.5%, ticked down from 62.6%.

Average hourly earnings rose 0.4% mom, above expectation of 0.3% mom. Over then past 12 months, average hourly earnings rose 4.0% yoy.

Canada’s employment grows 51k in Nov, unemployment rate jumps to 6.8%

Canada’s employment grew 51k in November, above expectation of 25k. Employment gains were concentrated in full-time work (+54k).

Employment rate was unchanged at 60.6%. Unemployment rate jumped from 6.5% to 6.8%, as more people are looking for work. Labor force participation rate rose 0.3% to 65.1%.

Total hours worked was down slightly by -0.2% mom but up 1.9% yoy. Average hourly wages grew 4.1% yoy, slowed from 4.9% yoy in October.

BoE’s Dhingra calls for more policy relief, labels current stance very restrictive

BoE MPC member Swati Dhingra, often viewed as the most dovish voice within the committee, reinforced her call for policy easing during an interview with Bloomberg TV today.

Dhingra highlighted the “very restrictive stance” of current monetary policy, arguing that high interest rates are dampening consumption, investment, and supply capacity. She stressed, “We should be easing policy more” to alleviate the strain on living standards and pave the way for economic normalization.

Dhingra pointed to easing wage pressures and declining service inflation as key indicators supporting a shift towards lower rates.

She advocated for a “gradual” approach to rate cuts, suggesting the Bank Rate should eventually settle between 2.5% and 3.5%, her updated estimate of the “neutral rate.” Notably, she acknowledged that this estimate has risen since BoE’s 2018 estimate of 2%-3%.

Turning to the potential fallout from a global trade war, Dhingra noted its indirect effects could significantly harm productivity and business adaptability. While she believes the direct impact on UK growth and inflation might be “limited,” she cautioned that secondary effects, such as supply chain disruptions and reallocation challenges, would be far more damaging.

Japan’s nominal wages growth hits multi-decade high, but real gains remain elusive

Japan’s labor market data for October showed nominal wages, or labor cash earnings, rose 2.6% yoy, in line with expectations. Regular pay, or base salary, grew 2.7% yoy, marking the fastest increase since November 1992. Full-time workers saw an even sharper wage rise at 2.8% yoy, the highest increase since comparable records began in 1994. Overtime pay also rebounded, registering a 1.4% yoy growth compared to a -0.9% decrease in the prior month.

However, real wages—adjusted for inflation—was stagnant, showing no change from a year ago. This followed declines of -0.4% and -0.8% yoy in September and August, respectively. The inflation rate used by Japan’s labor ministry for these calculations, excluding owners’ equivalent rent, slowed to 2.6%, the lowest in nine months.

On the household front, spending fell -1.3% yoy, better than the forecasted -2.6% yoy decline but still reflecting cautious consumer behavior. Food expenditures, comprising around 30% of total spending, dropped -0.8% yoy. Other categories faced sharper declines, including a -13.7% yoy plunge in clothing and shoes, a -10.7% yoy drop in housing-related expenditures, and a -14.0% yoy decrease in education spending, such as tuition fees.

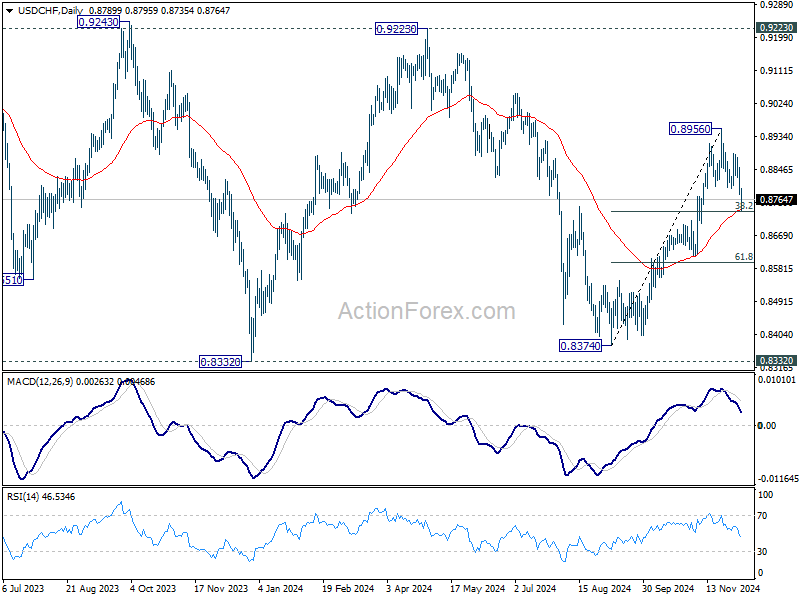

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8758; (P) 0.8806; (R1) 0.8832; More…

USD/CHF’s fall from 0.8956 short term top extends lower in early US session and touched 55 D EMA (now at 0.8737. Strong support could be seen from current level, and firm break of 0.8796 resistance will turn bias back to the upside for rebound. However, considering head and shoulder top pattern, firm break of the EMA will argue that whole rise from 0.8401 might have completed, and bring deeper decline to 61.8% retracement of 0.8401 to 0.8956 at 0.8613 next.

In the bigger picture, price actions from 0.8332 (2023 low) are currently seen as a medium term corrective pattern. Rise from 0.8374 is seen as the third leg. Overall outlook will continue to stay bearish as long as 0.9223 resistance holds. Break of 0.8332 low is in favor at a later stage when the consolidation completes.