Last week’s financial markets were characterized by a mix of resilience, speculation, and divergent central bank signals.

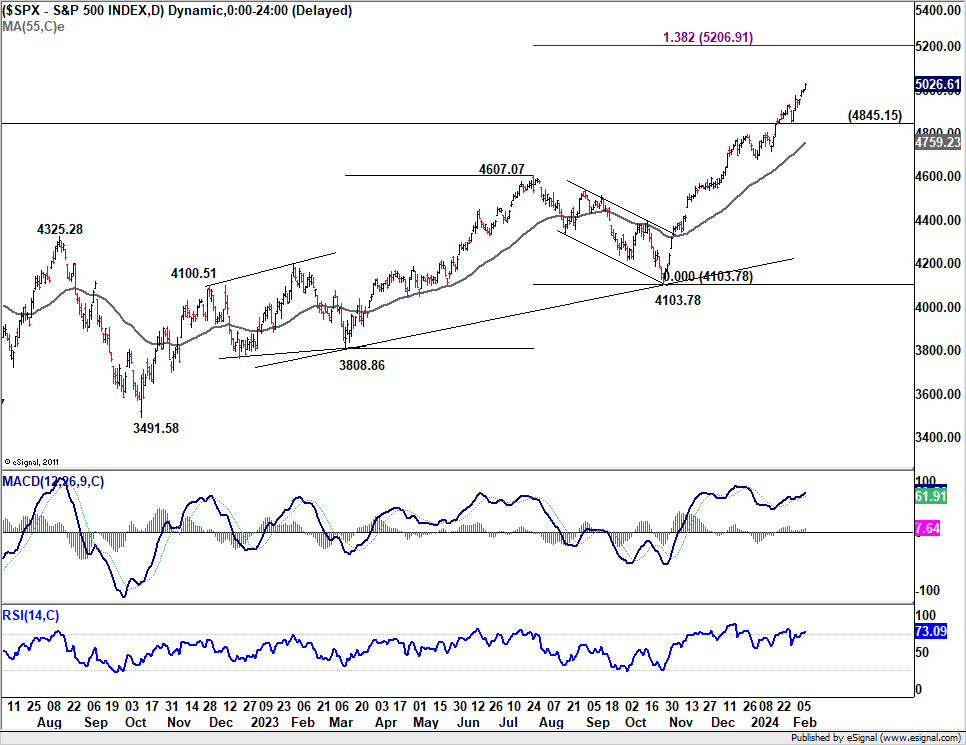

In the US, the narrative remained steadfast with Fed officials emphasizing a patient approach towards monetary policy, firmly pushing back against the market’s eager anticipations for imminent rate cuts. This cautious did little to dampen the spirits of investors, who propelled S&P 500 past the landmark 5000 level for the first time, a testament to the enduring optimism surrounding US economy’s resilience.

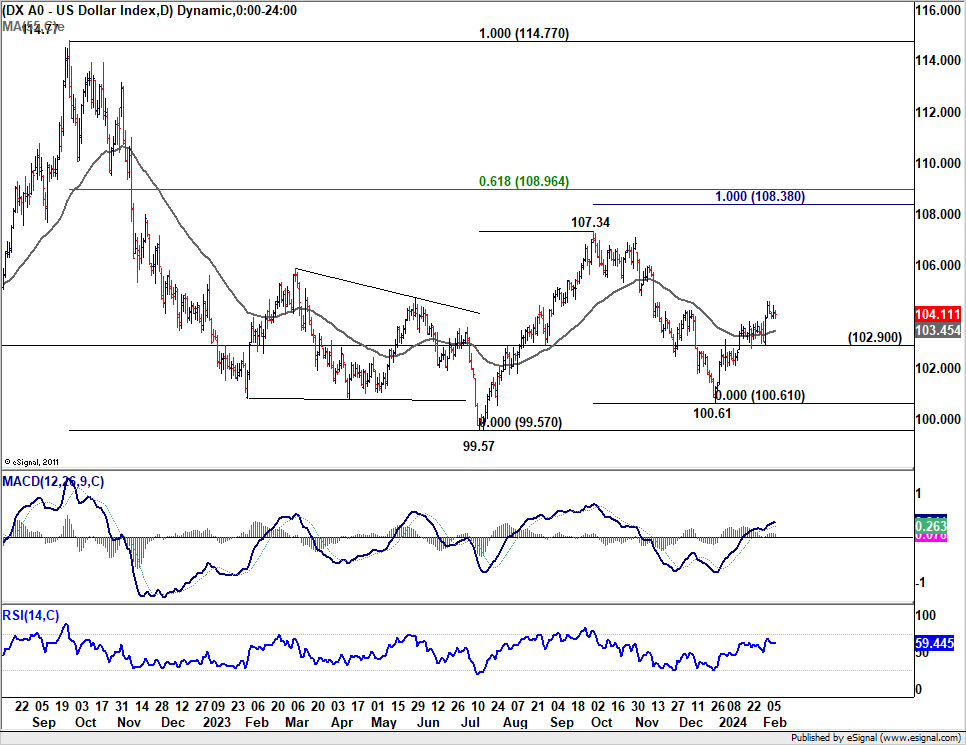

The ascent of S&P 500 was coupled with slight uptick in 10-year yield. While Dollar Index made strides, reflecting some progress, the greenback’s performance was notably middling when juxtaposed with its global counterparts.

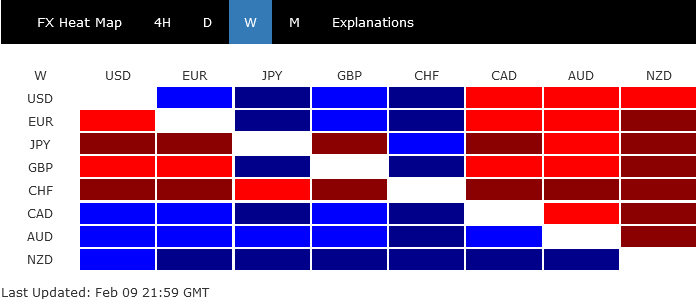

In Europe, Swiss Franc bore the brunt of the market’s recalibrations, finding itself at the bottom of the performance ladder. This position was influenced by similar cautionary messages from ECB and BoE regarding premature rate cut expectations. Nevertheless, Euro and Sterling ended the week on a slightly softer note against others.

Over to Asia, Japan presented a contrasting scenario, where a top BoJ official attempted to moderate expectations for aggressive policy tightening. This effort led to widespread sell-off in Yen, positioning it as the week’s second weakest. But at the time same, Nikkei also soared to new 34-year highs, buoyed by anticipation of continued loose monetary policy.

Commodity currencies emerged as the clear frontrunner amidst this global backdrop. New Zealand Dollar, in particular, stood out, riding high on the wave of speculation that RBNZ would implement further rate hikes. Australian Dollar, while also firming, trailed in the wake of RBA’s noncommittal stance on future rate adjustments. Canadian Dollar, despite a fleeting post-employment data rally, settled into the third spot

Market Optimism Prevails as S&P 500 Breaks 5000 Mark

US stock market soared remarkably again last week, marking its fifth consecutive winning streak and the 14th positive week out of the last 15, reflecting investor confidence in the resilience of the US economy. Despite Federal Reserve officials tempering expectations for an early interest rate cut, indicating rates might hold steady at least until Q2, market participants remain unfazed. The question now arises: will the ongoing bullish runs in stocks trigger fear of missing out sentiment, fueling further risk-on rallies?

Minneapolis Fed President Neel Kashkari introduced an interesting perspective with his essay, arguing that current monetary policy might not be as restrictive as previously thought. He attributed the rapid decline in inflation primarily to supply-side improvements rather than deceleration in economic activity (as seen in the strong consumption and labor market data). This interpretation allows for more extended period to assess the economy’s health before starting rate cut, without the risk of overly tight policy hindering growth.

Overall, Fed officials emphasized the need for further evidence of disinflation progress, particularly more broadening slowdown in price growth, before considering gradual easing of policy. At the same time, factors such as resilient consumer spending, robust job market, and global tensions present risks to inflation outlook.

S&P 500 closed at record high at 5026.61 last week. There might be some brief struggles to sustain above 5000 psychological level initially. But near term outlook will stay bullish as long as 4845.15 support holds. Next target is 138.2% projection of 3808.86 to 4607.07 from 4103.78 at 5206.91.

10-year yield extended the near term rebound to close at 4.187 last week. At this point, strong resistance is still expected from 38.2% retracement of 4.997 to 3.785 at 4.247 to limit upside. Price actions from 3.785 are seen as a sideway consolidation pattern that would extend for a while before downside breakout happens.

However, sustained break of 4.247 would indicate some important change in the fundamental outlook, probably on expectations that Fed’s interest rate would settle at a higher level during the upcoming rate cut cycle. In this case, 10-year yield could rally further to 61.8% retracement at 4.534.

Dollar index’s rally from 100.61 progressed as expected, even though just a small step. Further rise is expected as long as 102.90 support holds. Rise from 100.61 is seen as the third leg of the consolidation pattern from 99.57. Next target is 107.34 resistance.

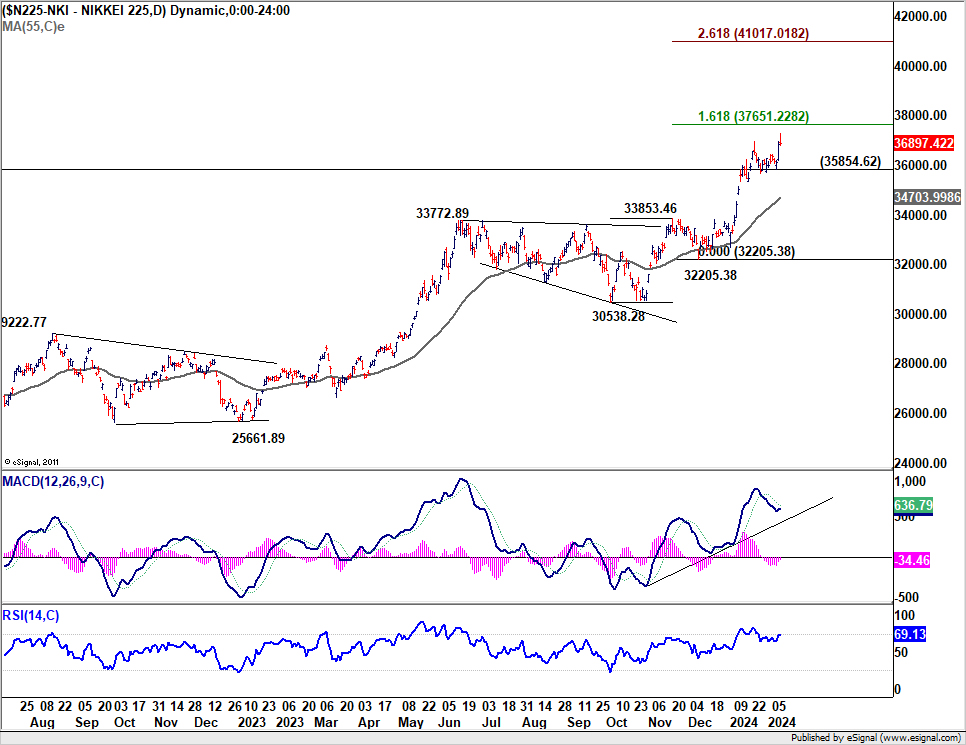

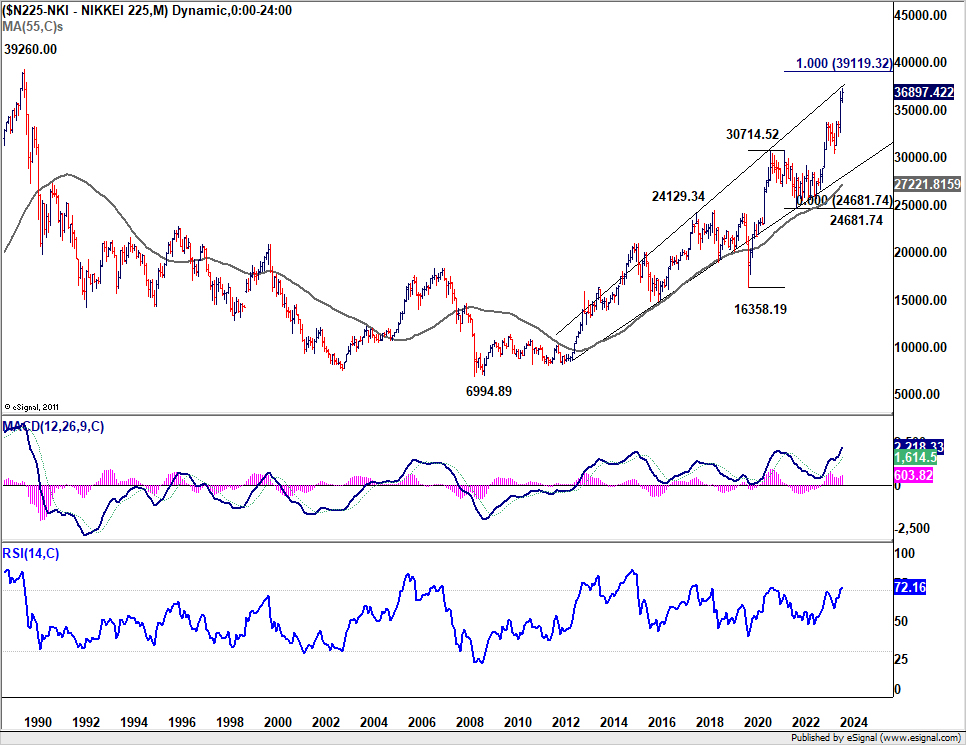

BoJ’s Dovish Stance Catapults Nikkei to New Heights, Yen Continues to Weaken

Japan’s stock market also jumped last week, with Nikkei hitting a new 34-year high. The surge, fueled by strong corporate earnings and expectations of continued loose monetary The robust optimism was partly driven by impressive earnings from major companies like SoftBank, Nintendo, and Toyota. Meanwhile, anticipation of continuous loose monetary policy and the persistently weak Yen also played an import part.

A key factor contributing to Nikkei’s surge was the speech by BoJ Deputy Governor Shinichi Uchida, who suggested that the central is unlikely to engage in aggressive interest rate hikes even after the cessation of its negative interest rate policy. Uchida’s remarks underscore the distinct economic conditions in Japan compared to the US and Europe, arguing against drawing parallels in interest rate outlooks among these regions.

Uchida highlighted the divergence in inflation levels, noting that while Fed and ECB initiated interest rate increases in 2022 amidst inflation rates above 8%, Japan’s inflation scenario is markedly different. Additionally, He emphasized the need for continued accommodative monetary policy to elevate medium- to long-term inflation expectations, which is still in the process of climbing to 2%.

Technically, near term outlook in Nikkei will now stay bullish as long as 35854.62 support holds. Next near term target is 161.8% projection of 30538.28 to 33853.46 from 32205.38 at 37651.22. Next medium term target is 100% projection of 16358.19 to 30714.52 from 24681.74 at 39119.32, which is close to 39260 record high made in 1990.

Yen, meanwhile, emerged as the second-worst performer last week, influenced by delayed rate cut expectations among major central banks and the anticipation of gradual tightening by BoJ. Rising yields globally and the prevailing risk-on sentiment have further pressured Yen. Despite this, Japan’s verbal interventions have been moderate so far. However, any intensification in the Yen’s decline could prompt more assertive responses from Japanese authorities.

NZD/JPY was one of the biggest movers last week, losing -2%. The strong break of 91.50 resistance confirmed long term up trend resumption. Outlook will now stay bullish as long as 90.70 resistance turned support holds. Next target is 61.8% projection of 80.42 to 89.67 from 86.75 at 92.46.

Considering bearish divergence condition in D MACD. Strong resistance could be seen from 92.46 projection level to limit upside, at least on first attempt. However, decisive break through could prompt upside acceleration to 100% projection at 96.00.

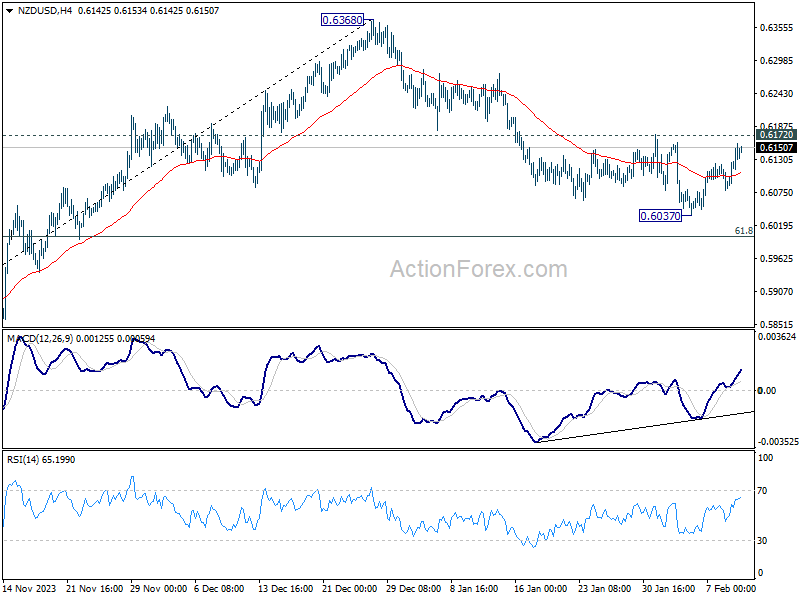

NZD Rallies Amid Rate Hike Buzz, Orr’s Upcoming Remarks to Set the Tone

Talking about New Zealand Dollar, it was surprisingly the standout currency last week, buoyed by anticipations of two more rate hikes by RBNZ in February and April, as suggested by ANZ’s forecasts. Chief Economist Sharon Zollner highlighted a series of “small but pretty consistent” economic data surprises that, in her view, bolster the case for further monetary tightening.

Contrastingly, Westpac presented a more cautious perspective, pointing to softer-than-anticipated GDP and inflation figures since RBNZ’s November Monetary Policy Statement. They argue for a pause by RBNZ throughout 2024, positing that the upcoming statement could set the stage for a possible rate increase within the next six months, contingent upon core inflation pressures subsiding sufficiently.

The stage is set for an intriguing development on Monday when RBNZ Governor Adrian Orr and Deputy Governor Christian Hawkesby are scheduled to speak before the parliament’s Finance and Expenditure Committee. Though the session’s official agenda focuses on the Financial Stability Report, it inadvertently provides a platform for Orr to directly address the evolving market expectations regarding monetary policy. The remarks made during this session have the potential to significantly sway market sentiment, either reinforcing the bullish momentum behind New Zealand Dollar or introducing a note of caution that tempers market enthusiasm.

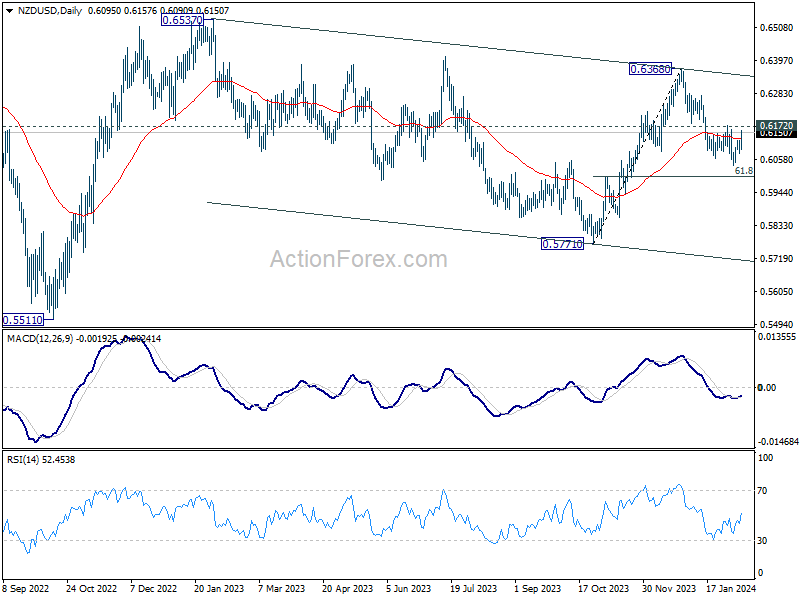

NZD/USD’s decline from 0.6368 halted after hitting 0.6037, but recovery is capped below 0.6172 resistance so far. Another decline remains in favor, and break of 0.6037 would resume the fall towards 0.5771 low, as part of the whole down trend from 0.6537.

However, considering bullish convergence condition in 4H MACD, strong break of 0.6172 will dampen the above bearish view, and argue that the decline from 0.6368 has completed. Stronger rebound would then be seen back towards this resistance. We’d probably know which way it goes on Monday.

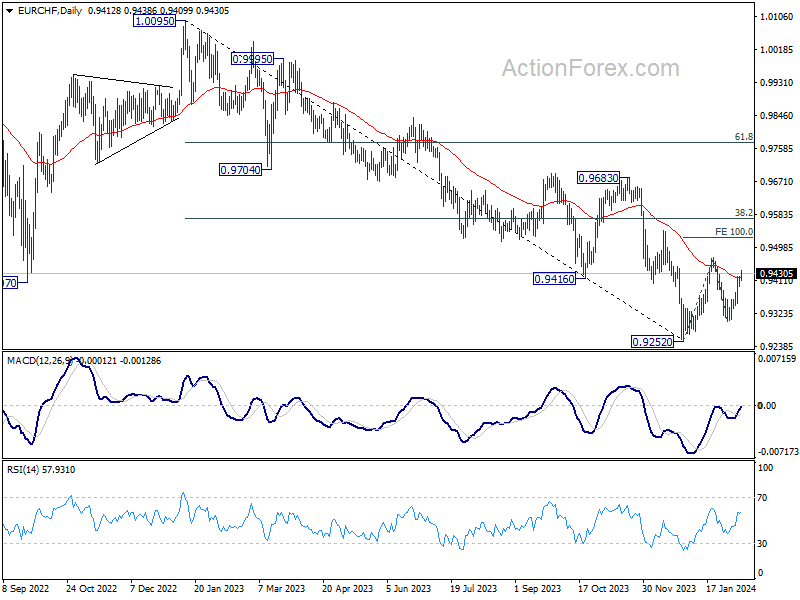

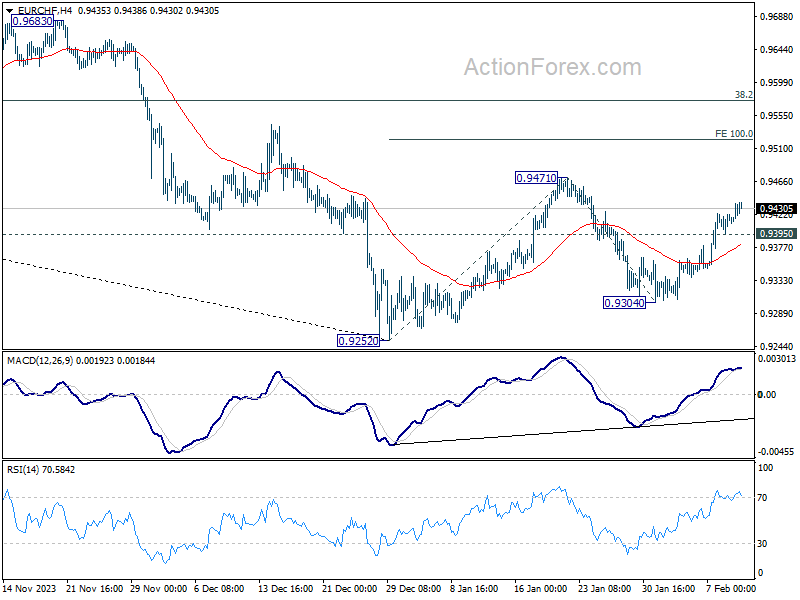

EUR/CHF Weekly Outlook

EUR/CHF’s rebound last week suggests that pull back from 0.9471 has completed at 0.9304 already. Initial bias remains on the upside this week for 0.9471. Firm break there will resume whole rebound from 0.9252 to 100% projection of 0.9252 to 0.9471 from 0.9304 at 0.9523. On the downside, below 0.9395 minor support will turn intraday bias neutral first.

In the bigger picture, price actions from 0.9252 are tentatively seen as a correction to the five-wave down trend from 1.0095 (2023 high). Further rise would be seen to 38.2% retracement of 1.0095 to 0.9252 at 0.9574. But overall medium term outlook will remain bearish as long as 0.9683 resistance holds.

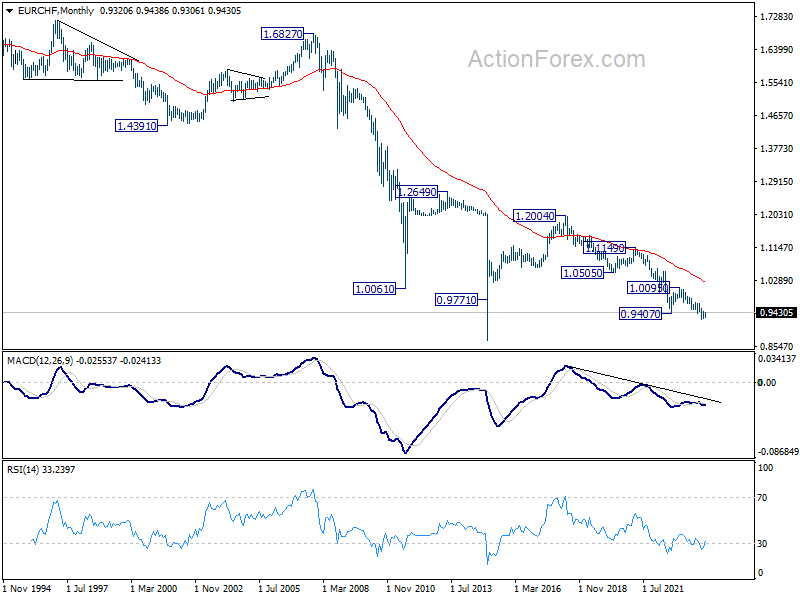

In the long term picture, fall from 1.2004 (2018 high) is part of the multi-decade down trend. Firm break of 1.0095 resistance is needed to be the first sign of long term bottoming. Otherwise, outlook will remain bearish.