The selloff in Yen remains the major theme in the market today, but both Dollar and Euro are also now under some pressure. For now, New Zealand Dollar is winning the race, followed by Aussie and Sterling. Swiss Franc and Canadian Dollar are mixed. In other markets, major European indexes are trading slightly in black, so are US futures. Europe and US benchmark treasury yields are extending rally.

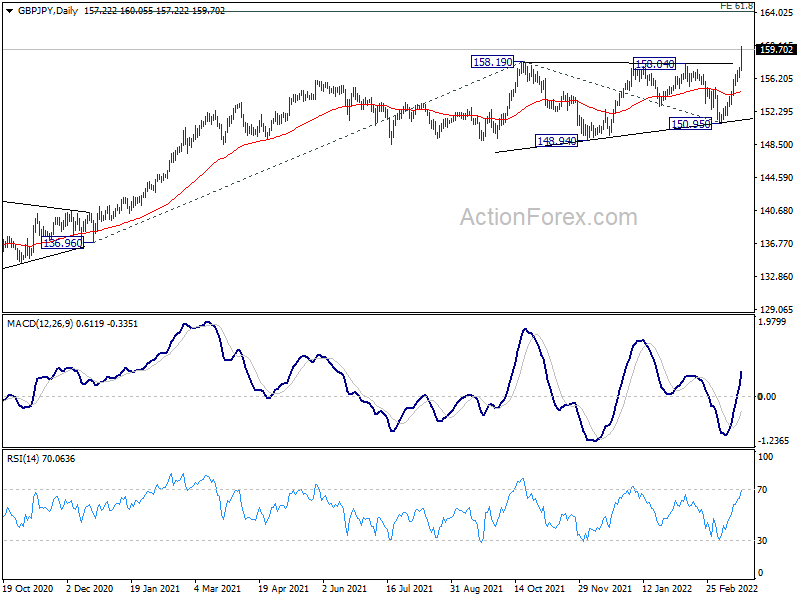

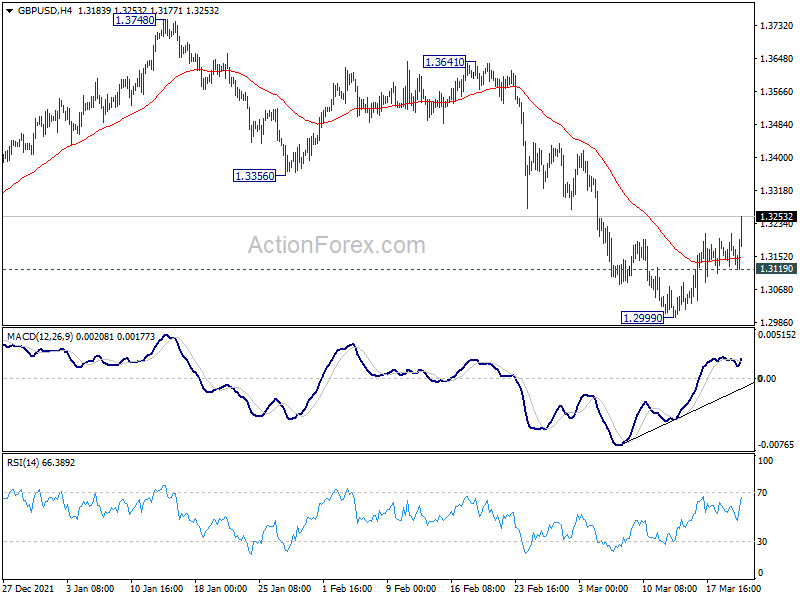

Technically, Sterling is displaying some strength today. EUR/GBP’s break of 0.8358 minor support suggests completion of rebound from 0.8201. Deeper fall would be seen back to retest this low. GBP/USD’s break of 1.3210 minor resistance suggest resumption of rebound from 1.2999, for 55 day EMA at 1.3361. GBP/JPY also break through 158.19 resistance decisively to resume medium term up trend.

In Europe, at the time of writing, FTSE is up 0.51%. DAX is up 0.78%. CAC is up 0.75%. Germany 10-year yield is up 0.055 at 0.525. Earlier in Asia, Nikkei rose 1.48%. Hong Kong HSI rose 3.15%. China Shanghai SSE rose 0.19%. Singapore Strait Times dropped -0.16%. Japan 10-year JGB yield rose 0.0111 to 0.219.

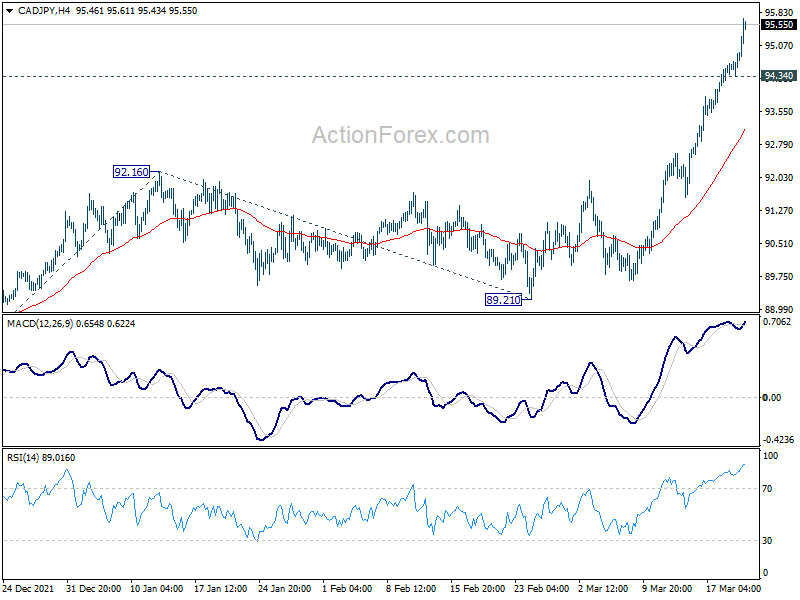

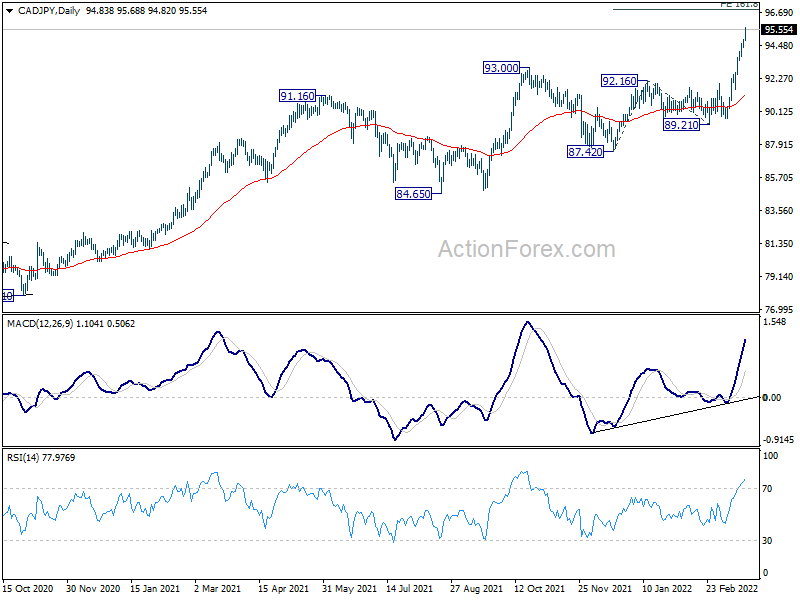

CAD/JPY marches higher, targeting 96.87 next

CAD/JPY’s rally accelerates again today and hits as high as 95.68. Further rise is expected as long as 94.34 minor support holds. Next near term target is 161.8% projection of 87.42 to 92.16 from 89.21 at 96.87 next. Below 93.34 minor support will bring consolidations, but retreat should be contained above 92.16 resistances turned support to bring up trend resumption.

Also, noted that the up trend from 73.80 could either be a leg inside the pattern from 68.38, or the start of a long term up trend. Hence, 106.48 high is the next medium term target.

ECB de Guindos: No stagflation, inflation expectations not deanchored

ECB Vice President Luis de Guindos said today, “we can so far dismiss the possibility of stagflation because even in the weakest scenario we are looking at growth of around 2% in 2022.”

De Guindos also said higher energy prices are pushing inflation to record high. However, There is no indication that inflation expectations are becoming “deanchored”.

ECB Villeroy: We should not overreact to short-term volatility in energy prices

ECB Governing Council member Villeroy de Galhau said today, “it is indeed time to take our foot off the accelerator, as decided during our last governing council.”

“That said, we should not overreact to short-term volatility in energy prices, and instead focus more on underlying inflation and on the medium term,” he added.

BoJ Kuroda: We need to patiently maintain our powerful monetary easing

BoJ Governor Haruhiko Kuroda reiterated to the parliament today that it’s still premature to discuss details on stimulus exit. “Given recent price developments, we need to patiently maintain our powerful monetary easing,” he said.

Kuroda said consumer prices are likely to rise. However, he warned that “instead of leading to higher wages and corporate profits, such cost-push inflation will weigh on the economy in the long run by hurting corporate profits and households’ real income.”

New Zealand Westpac consumer confidence dropped to 92.1, lowest since 2008

New Zealand Westpac consumer confidence dropped from 99.1 to 92.1 in Q1, hitting the lowest level since the global financial crisis in 2008. Present conditions index dropped from 94.8 to 90.1. Expected conditions index dropped from 101.9 to 93.5. One-year economic outlook dropped from -11.2 to -22.8. Five-year economic outlook dropped from 10.0 to 0.8.

Westpac said:”Households have reported that their financial position has deteriorated as the economy has been buffeted by a multitude of headwinds. That includes rising consumer prices and higher mortgage rates, both of which are squeezing households’ disposable incomes. The rapid spread of Omicron is also likely to have dampened confidence in recent weeks.

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3127; (P) 1.3169; (R1) 1.3210; More…

GBP/USD’s break of 1.3210 minor resistance confirms short term bottoming at 1.2999. Intraday bias is back on the upside for rebound to 55 day EMA (now at 1.3361). On the downside, break of 1.3119 minor support will turn intraday bias back to the downside for retesting 1.2999. Firm break there will resume larger down trend from 1.4248.

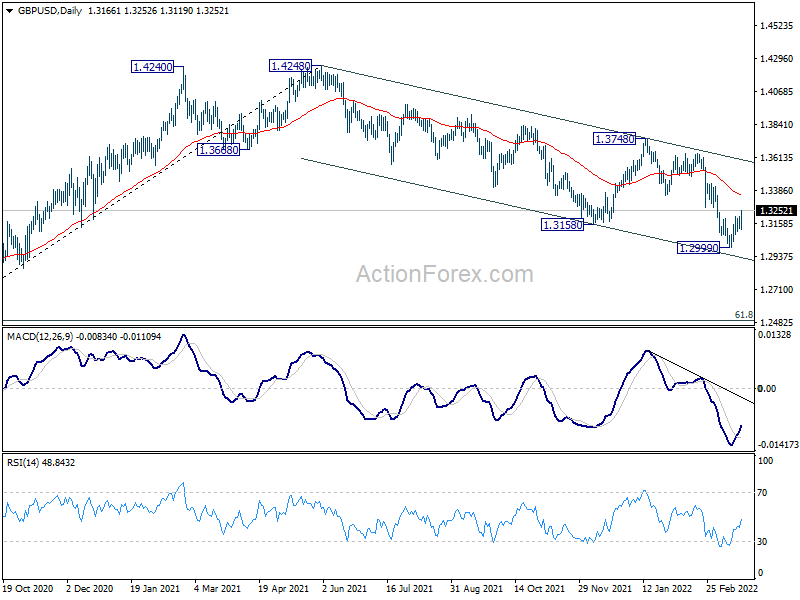

In the bigger picture, current development suggests that the up trend from 1.1409 (2020 low) has completed at 1.4248. Decline from 1.4248 could still be a corrective move, or it could be the start of a long term down trend. In either case, deeper decline would be seen back to 61.8% retracement of 2.1161 to 1.1409 at 1.2493. In any case, break of 1.3748 resistance is needed to indicate medium term bottoming, or outlook will stay bearish.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 20:00 | NZD | Westpac Consumer Survey Q1 | 92.1 | 99.1 | ||

| 07:00 | GBP | Public Sector Net Borrowing (GBP) Feb | 12.3B | -4.5B | -3.7B | -7.8B |

| 09:00 | EUR | Eurozone Current Account (EUR) Jan | 23.0B | 24.3B | 22.6B | |

| 12:30 | CAD | Industrial Product Price M/M Feb | 3.10% | 1.20% | 3.00% | |

| 12:30 | CAD | Raw Material Price Index M/M Feb | 6.00% | -0.60% | 6.50% |